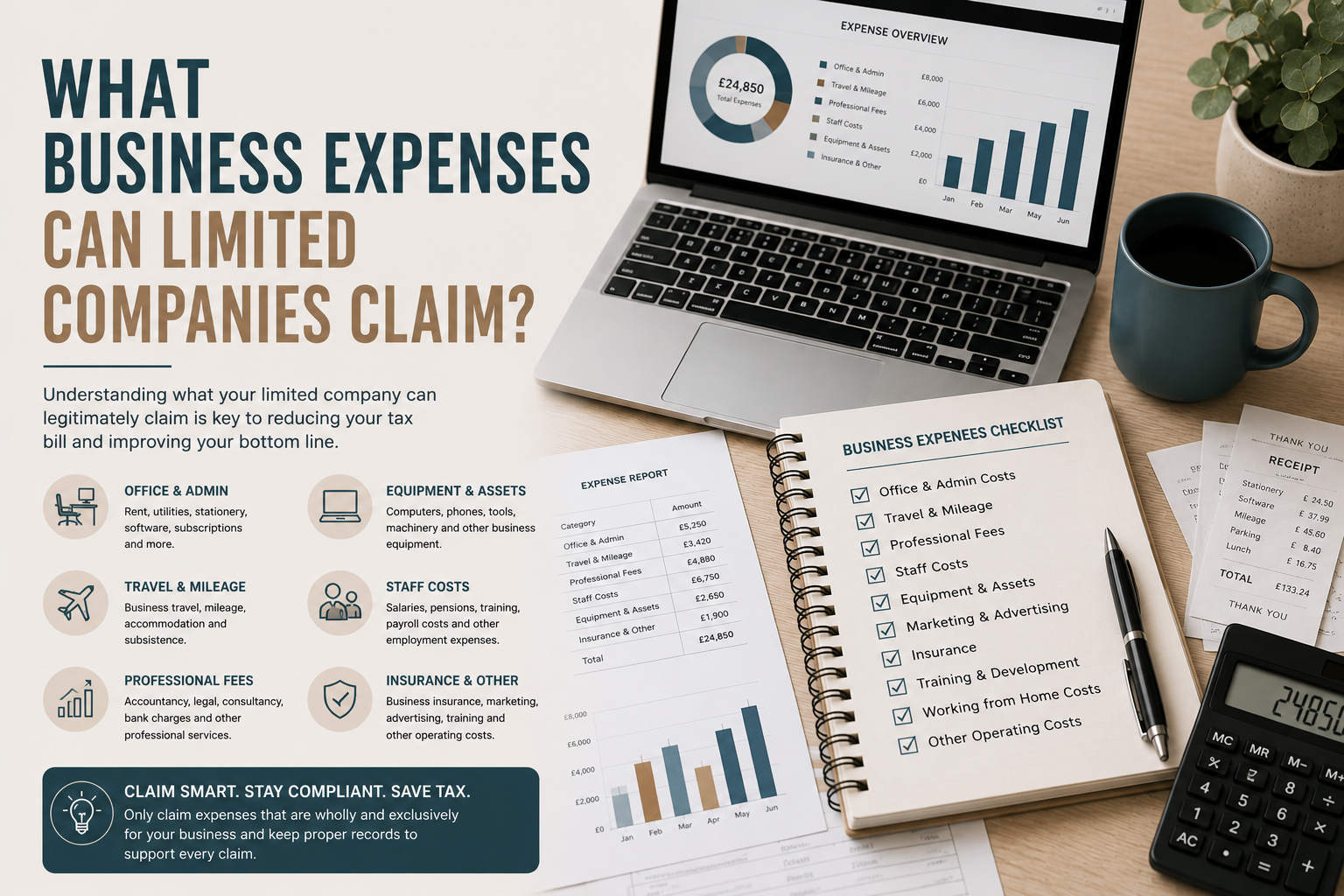

What Business Expenses Can Limited Companies Claim?

A Practical UK Guide for Company Directors

Claiming business expenses correctly is one of the simplest ways to reduce a limited company’s tax bill legally.

But it is also an area where many directors make mistakes.

Some directors miss legitimate costs because they are unsure what can be claimed. Others put personal spending through the company and assume the accountant can “sort it out later”.

The correct approach sits between the two.

A limited company can usually deduct the costs of running the business when calculating taxable profit before Corporation Tax. However, the expense must be genuinely business-related and properly recorded. GOV.UK confirms that limited companies can deduct the costs of running the business when working out taxable profit before Corporation Tax.

This guide explains the common categories of limited company expenses, the grey areas directors should watch, and how to avoid common mistakes.

The Basic Rule: Wholly and Exclusively for Business

The key principle is that expenses must be incurred for the purposes of the company’s trade.

HMRC’s guidance refers to the “wholly and exclusively” test. For companies, the statutory restriction is in Corporation Tax Act 2009, and expenditure is not deductible unless it is incurred wholly and exclusively for the purposes of the trade, profession or vocation.

In simple terms:

If the expense is genuinely for the business, it may be allowable.

If it has a personal purpose, it may be disallowed, partly disallowed, treated as a benefit, or posted to the director’s loan account.

Practical Example

A company pays for accounting software used entirely for business bookkeeping.

That is likely to be a business expense.

But if the company pays for the director’s family holiday and describes it as a “business trip” without genuine business purpose and evidence, that is unlikely to be allowable.

1. Accountancy and Professional Fees

A limited company can usually claim fees for services connected to the business, such as:

- annual accounts

- Corporation Tax returns

- bookkeeping

- VAT returns

- payroll

- management accounts

- business tax advice

- company secretarial support

- legal advice relating to the business

Important Distinction

Advice for the company is different from personal advice for the director.

For example:

- company accounts and Corporation Tax advice: usually company expense

- personal tax return for the director: may need separate treatment

- personal mortgage advice: not a company expense

Where a bill covers both company and personal work, it should be split correctly.

2. Office Costs and Business Administration

Common office and admin costs may include:

- stationery

- printing

- postage

- business bank charges

- office supplies

- business software

- cloud storage

- business phone systems

- professional subscriptions where relevant to the business

Practical Example

A company pays for QuickBooks, Xero, Microsoft 365, secure cloud storage and business email hosting.

These are generally business expenses where they are used for the company.

3. Software and Subscriptions

Many modern businesses rely on subscriptions.

Examples may include:

- bookkeeping software

- payroll software

- CRM systems

- project management tools

- website hosting

- email marketing software

- payment processing tools

- industry-specific platforms

These are often allowable if used for the business.

Common Mistake

Directors sometimes run personal subscriptions through the company.

Examples may include personal streaming services, family apps, personal storage accounts or non-business memberships.

If the subscription is not genuinely for the company, it should not simply be treated as a business expense.

4. Business Premises Costs

If your company rents or operates from business premises, possible expenses may include:

- rent

- business rates

- utilities

- office insurance

- cleaning

- repairs and maintenance

- security

- broadband

Watch the Difference Between Repairs and Improvements

Repairs are generally different from improvements.

For example:

- repairing an existing office door may be a repair

- building a new extension or significantly improving premises may be capital in nature

Capital costs may not be deducted in the same way as normal running costs.

5. Working From Home Costs

Many directors work from home, either full-time or partly.

A company may be able to reimburse reasonable additional household costs where the director or employee works from home under proper arrangements. HMRC’s Employment Income Manual refers to employer payments for homeworking expenses and confirms that £6 per week or £26 per month can be agreed for monthly paid employees without the employer having to justify the amount, provided the relevant conditions are met.

Examples of Additional Costs

This may include a reasonable contribution towards:

- heating

- electricity

- business telephone calls

- internet costs where properly evidenced

Practical Example

A director works from home regularly and the company pays £26 per month as a homeworking allowance.

This may be simple and practical, but the company should still keep clear records and ensure the arrangement is reasonable.

Be Careful With Rent Charged to the Company

Some directors consider charging rent to their company for using part of their home.

This can work in some cases, but it needs care because it may create:

- personal rental income

- Self Assessment reporting

- possible capital gains tax complications later if part of the home is used exclusively for business

- administrative complexity

For many small companies, a modest homeworking allowance is simpler.

6. Travel Costs

A company can usually claim genuine business travel costs.

Examples may include:

- train fares

- flights for business trips

- hotel accommodation for business travel

- parking

- taxis

- mileage claims for business journeys

- tolls and congestion charges for business travel

Ordinary Commuting Is Not Usually Allowable

Travel between home and a permanent workplace is generally ordinary commuting and does not qualify for tax relief. HMRC guidance states that an employee cannot have tax relief for ordinary commuting or private travel.

Practical Example

A director travels from their home office to visit a client.

That may be business travel.

But if the director travels daily from home to the company’s regular office, that is likely to be ordinary commuting.

7. Mileage Claims

If a director uses their personal car for business journeys, the company may reimburse business mileage.

This is often cleaner than putting a personal car through the company.

Mileage claims should be supported by records, such as:

- date of journey

- start and end location

- business purpose

- number of miles

- client or project reference

Common Mistake

Directors claim fuel costs but do not keep mileage records.

This creates weak evidence if HMRC asks questions.

8. Company Cars and Vans

A limited company can buy or lease vehicles, but this area needs careful advice.

The tax treatment depends on:

- whether it is a car or van

- whether there is personal use

- CO₂ emissions

- whether it is electric

- whether it is leased or purchased

- VAT recovery rules

- benefit-in-kind implications

HMRC’s Corporation Tax guidance confirms that companies may be able to claim capital allowances on business assets such as equipment, machinery and business vehicles, but anything directors or employees get personal use from must be treated as a benefit.

Practical Example

A director buys a petrol car through the company and uses it personally.

The company may get some tax relief, but the director may face a benefit-in-kind charge, and the overall position may be worse than personal ownership plus mileage claims.

Electric cars can be more attractive in some cases, but the figures should still be modelled properly.

9. Equipment, Tools and Machinery

Companies often buy assets such as:

- computers

- laptops

- printers

- office furniture

- tools

- machinery

- cameras

- phones

- tablets

- specialist business equipment

These may qualify for capital allowances rather than being deducted as ordinary day-to-day expenses.

The Annual Investment Allowance allows businesses to deduct the full value of qualifying items from profits before tax, subject to the AIA rules and limits. GOV.UK states that AIA can be claimed on most plant and machinery up to the AIA amount, and the main AIA limit is currently £1 million.

Practical Example

A design company buys a high-spec computer used wholly for business.

This may qualify for capital allowances.

If the same computer is used significantly by the director’s family for personal use, the treatment may be different and should be reviewed.

10. Mobile Phones and Internet

Mobile phones and internet costs can be allowable, but personal use needs to be considered.

Company Mobile Phone

A company-provided mobile phone can often be treated favourably if structured properly.

Personal Mobile Phone

If the director uses a personal phone partly for business, only the business element should be considered.

Internet

If the internet is used both personally and for business, the company should not simply claim the whole household bill unless it is genuinely a separate business connection or properly supported.

11. Marketing and Advertising

Marketing costs are usually allowable where they are for the business.

Examples include:

- website design

- website hosting

- SEO services

- Google Ads

- social media advertising

- brochures

- business cards

- photography

- branding

- email marketing

- sponsorships with a genuine business purpose

Practical Example

A company pays for a new website, blog content and SEO work to attract customers.

These are generally business costs.

However, if the company pays for a personal social media campaign unrelated to the business, that would not be treated the same way.

12. Training and Development

Training costs may be allowable where they relate to the company’s trade and help the director or employees perform their role.

Examples may include:

- software training

- technical updates

- CPD courses

- industry training

- safety training

- business skills relevant to the company

Be Careful With New Skills

Training that updates existing skills is usually easier to justify than training for a completely new trade or personal career change.

Practical Example

An accountancy practice pays for tax update training.

That is clearly connected to the business.

A construction company paying for a director’s unrelated personal hobby course would be much harder to justify.

13. Staff Costs and Payroll

Limited companies can usually claim staff employment costs, such as:

- salaries

- employer National Insurance

- employer pension contributions

- staff training

- recruitment costs

- payroll processing costs

Director Salaries

Director salaries are generally company expenses where properly processed through PAYE.

However, salary planning should be reviewed carefully alongside dividends, Corporation Tax, National Insurance and the director’s personal tax position.

14. Pension Contributions

Employer pension contributions can be a valuable planning tool for company directors.

Where contributions are made by the company and meet the relevant rules, they may reduce taxable company profits.

However, pension planning should consider:

- annual allowance

- available profits

- commercial justification

- the director’s wider pension position

- timing of contributions

This is one of the areas where advice before payment is important.

15. Insurance

Common business insurance costs may include:

- professional indemnity insurance

- public liability insurance

- employer’s liability insurance

- office insurance

- cyber insurance

- business equipment insurance

- relevant business vehicle insurance

These are generally allowable where they protect the business.

Personal Insurance

Personal life insurance, private health cover or personal protection policies may have different tax treatment and could be taxable benefits depending on the arrangement.

16. Business Entertaining

This is one of the most misunderstood areas.

Client entertaining may be a genuine business cost in accounting terms, but it is generally not deductible for Corporation Tax.

Examples include:

- taking clients for lunch

- event hospitality

- tickets to sporting events

- drinks with clients

Practical Example

A company takes a prospective client out for dinner to discuss a potential contract.

The cost may be paid by the business and recorded in the accounts, but it is usually disallowed when calculating Corporation Tax.

This means it does not reduce the company’s taxable profit.

17. Staff Entertainment

Staff entertainment can be treated differently from client entertaining.

An annual staff event, such as a Christmas party, may qualify for favourable treatment if the conditions are met.

However, it must be:

- open to staff generally

- annual in nature

- within relevant limits

- properly documented

Where the company has only directors and no staff, the position should still be reviewed carefully.

18. Trivial Benefits

Trivial benefits can be a useful but often misunderstood area.

HMRC says a benefit can be treated as trivial where it costs £50 or less, is not cash or a cash voucher, is not a reward for work or performance, and is not in the employee’s contract. If the conditions are met, there is no tax or National Insurance to pay and the benefit does not need to be reported to HMRC.

Important Director Limit

For close companies, there are additional rules and an annual cap for directors and office holders. This should be checked before relying on trivial benefits.

Practical Example

A company gives a director a £40 birthday gift voucher that is not cash, not performance-related and not contractual.

This may qualify as a trivial benefit if the conditions are met.

A £200 reward for hitting a sales target would not qualify.

19. Gifts

Business gifts can be allowable in limited circumstances, but the rules are restrictive.

The treatment depends on:

- who receives the gift

- cost

- whether it includes food, drink, tobacco or vouchers

- whether it includes advertising

- whether it is a reward or benefit

Because the rules are easy to get wrong, gifts should be reviewed before being claimed.

20. Clothing

Ordinary clothing is usually not allowable just because you wear it for work.

Allowable clothing is more likely to include:

- uniforms

- protective clothing

- branded workwear

- safety equipment

Practical Example

A director buys a normal suit for client meetings.

This is unlikely to be allowable because it has ordinary personal use.

A construction company buys branded high-visibility jackets and safety boots for site work.

That is much more likely to be allowable.

21. Food and Subsistence

Food and drink can be claimed in some business travel situations, but not simply because the director is working.

The position depends on whether the cost is linked to qualifying business travel, temporary workplace rules, or staff arrangements.

Common Mistake

A director claims daily lunch near their normal workplace as a business expense.

That is usually not allowable because everyone needs to eat, whether working or not.

22. Bank Charges, Interest and Finance Costs

Companies may be able to claim:

- business bank charges

- card processing fees

- loan interest for business borrowing

- hire purchase interest

- payment platform fees

However, borrowing must be for business purposes.

If the company borrows money and the funds are used personally by the director, the treatment becomes more complex.

23. Bad Debts

If a customer does not pay and the debt is genuinely bad, a company may be able to claim relief for that bad debt.

However, it should be properly evidenced.

Keep records showing:

- invoice raised

- attempts to collect payment

- correspondence

- reason debt is considered bad

- accounting treatment

24. Repairs and Maintenance

Repairs to business assets or premises may be allowable.

Examples include:

- repairing equipment

- fixing office furniture

- maintaining tools

- repairing business premises

But improvements or upgrades may be capital expenditure.

Practical Example

Repairing a broken laptop screen may be a repair.

Buying a new high-spec laptop may be a capital asset.

25. What Limited Companies Usually Cannot Claim

Common disallowed or problematic costs include:

- personal expenses

- ordinary commuting

- client entertaining

- fines and penalties

- personal clothing

- personal holidays

- non-business subscriptions

- excessive or unsupported claims

- dividends, because dividends are distributions of profit after tax rather than deductible expenses

This does not mean the company cannot pay for some of these items. It means the payment may not reduce taxable profits, or it may create a benefit, director’s loan account entry, or other tax issue.

Common Mistakes Directors Make With Expenses

1. Assuming the Company Bank Account Is Their Own Money

The company is a separate legal entity.

Company money is not automatically the director’s personal money.

2. Claiming Costs Without Receipts

Bank transactions alone are not always enough.

Receipts and invoices support the nature of the expense.

3. Ignoring VAT Treatment

An expense may be allowable for Corporation Tax but still have different VAT rules.

For example:

- some VAT may be blocked

- some suppliers may not be VAT registered

- some invoices may be invalid for VAT recovery

- some costs may be exempt or outside the scope

4. Leaving Expense Reviews Until Year-End

By the time the year-end accounts are prepared, it may be too late to correct poor habits easily.

5. Not Separating Personal and Business Spending

This creates bookkeeping problems and often leads to director’s loan account issues.

Record Keeping: What Evidence Should You Keep?

Limited companies must keep adequate accounting records. GOV.UK states that company records normally need to be kept for 6 years from the end of the last company financial year they relate to, and longer in some circumstances.

Keep:

- invoices

- receipts

- bank statements

- mileage logs

- contracts

- supplier statements

- payroll records

- VAT invoices

- board minutes where relevant

- notes explaining unusual expenses

Good records protect the company if HMRC asks questions.

Practical Scenario: Company Expenses Done Properly

A small limited company director works from home and visits clients.

The company pays for:

- bookkeeping software

- laptop

- business phone

- professional indemnity insurance

- website hosting

- accountancy fees

- mileage for client visits

- business stationery

- homeworking allowance

The director keeps:

- receipts

- mileage records

- invoices

- bank records

- notes of business purpose

This makes the accounts cleaner, reduces the risk of errors and helps ensure the company claims the expenses it is entitled to claim.

Practical Scenario: Company Expenses Done Poorly

Another director pays the following from the company account:

- personal groceries

- family meals

- personal holidays

- home broadband without apportionment

- petrol with no mileage records

- personal subscriptions

- client entertaining treated as deductible

- random cash withdrawals

At year-end, the bookkeeping becomes messy.

Some costs are disallowed. Some are posted to the director’s loan account. VAT may need adjusting. The director may also have taken more money from the company than expected.

This is exactly why expense discipline matters.

Related Blogs

- Director’s Loan Account Explained

- Dividends Explained for UK Company Directors

- Tax Efficient Profit Extraction for UK Company Directors

- How Much Salary Should a Director Take in 2026/27?

Frequently Asked Questions

Can a limited company claim expenses paid personally by the director?

Yes, if the expense was genuinely for the company and properly evidenced. The company can reimburse the director, or the cost can be credited to the director’s loan account.

Can my company pay for my mobile phone?

Potentially, but the structure matters. A company contract is usually cleaner than claiming personal phone costs. Personal use and contract ownership should be reviewed.

Can I claim clothing through my limited company?

Ordinary clothing is usually not allowable, even if worn for work. Uniforms, protective clothing and branded workwear may be allowable depending on the facts.

Can my company pay for lunch?

Sometimes, but not simply because you are working. Meals linked to qualifying business travel may be allowable, but ordinary daily meals are usually personal.

Can a limited company claim home office costs?

Yes, in some cases. A simple homeworking allowance may be possible, or actual additional costs can be considered if properly evidenced.

Can my company pay for client entertaining?

Yes, the company can pay, but client entertaining is usually disallowed for Corporation Tax, meaning it does not reduce taxable profits.

Can my company buy a car?

Yes, but company cars can create benefit-in-kind tax charges where there is personal use. The position depends heavily on the vehicle and usage.

Do I need receipts for every expense?

You should keep proper evidence. For many expenses, receipts or invoices are important because bank payments alone may not prove the business purpose.

How PR Accountants Can Help

At PR Accountants, we help limited company directors claim expenses correctly while staying compliant.

We support businesses with:

- bookkeeping

- VAT returns

- payroll

- Corporation Tax

- management accounts

- director salary and dividend planning

- director’s loan account reviews

- business expense reviews

- tax planning

Our focus is not just filing accounts. We help business owners understand what they can claim, avoid common mistakes and make better financial decisions.

Final Thoughts

Business expenses can reduce your company’s tax bill, but they need to be handled properly.

The best approach is simple:

- keep business and personal spending separate

- keep receipts and invoices

- review expenses regularly

- understand VAT treatment

- avoid guessing on grey areas

- get advice before making large purchases

Good expense management improves tax efficiency, bookkeeping accuracy and financial control.

Unsure Whether Your Company Is Claiming Expenses Correctly?

Incorrect expense claims can lead to tax issues, VAT errors and director’s loan account problems.

PR Accountants can help you clean up your bookkeeping, review your expenses and make sure your limited company is claiming what it is entitled to, without taking unnecessary risks.

👉 Contact PR Accountants today for practical, proactive accounting support for your limited company. Contact Us